Don't worry! The contents here will appear on the published page.

SaaS Accounting Explained: Revenue Recognition, Metrics & Best Practices (2026)

Woosung Chun

CFO, DualEntry

.jpg)

Woosung Chun

CFO, DualEntry

Woosung Chun is the CFO of DualEntry with experience in corporate finance, accounting, strategy, and acquisitions. He previously grew from scratch and led the M&A and Finance teams at Benitago, where he completed more than 12 acquisitions in 2 years. He graduated with a BS from NYU Stern. At DualEntry, Woosung writes about AI in accounting, revenue recognition, foreign currency accounting, hedge accounting, and ERP modernization for finance teams navigating complex, multi-entity environments.

Learn about our editorial policies.

Last updated

July 2, 2026

Reviewed by

Do San (Justin) Myung

Do San (Justin) Myung

Expert Accountant & Former Consulting CFO | DualEntry

Justin (Do San Myung) is Expert Accountant at DualEntry with 20+ years of hands-on experience managing general ledgers, financial close processes, and ERP implementations for mid-market and enterprise companies. As a former Consulting CFO and Controller, he has personally overseen month-end closes, SOX compliance programs, and multi-entity consolidations across technology, manufacturing, and services industries. Justin specializes in transforming manual accounting workflows into automated, AI-driven processes.

Learn about our editorial policies.

Summarize this article

SaaS accounting looks simple from the outside: sell software, collect subscriptions, report revenue. It’s actually very different from traditional accounting – and unfortunately, many SaaS companies only realize this when audits or board reporting reveal underlying issues.

The main problem? Timing. SaaS hinges on accrual accounting.¹ A SaaS business often collects cash upfront for an annual subscription, but it can’t recognize that full amount as revenue on day one. Instead, revenue is earned over the service period. This creates a cascade of accounting complexity across revenue recognition, deferred revenue journal entries, forecasting, metrics, and reporting. Setting up the right chart of accounts is the foundation for all of this -- use our SaaS chart of accounts setup guide to start.

SaaS companies deal with renewals, upgrades, downgrades, usage-based pricing, free trials, and multi-year contracts. This calls for a different financial system to businesses with “regular” accounting setups, which instead focus on one-time sales, inventory topics, and simpler billing cycles.

In this guide, we’ll go over how accounting for SaaS companies works in reality: from ASC 606 revenue recognition to deferred revenue and need-to-know metrics. Whether you’re interested in SaaS accounting as a founder, a finance lead, or an operator, you’ll find everything you need to get it right and avoid any reporting gaps.

What is SaaS accounting?

SaaS accounting is the set of financial practices specific to software-as-a-service businesses, where revenue is earned over time through subscriptions (rather than recognized at a single point of sale). This creates unique challenges around revenue recognition methods, deferred revenue, and financial reporting that day-to-day accounting methods don’t address.

How SaaS accounting is different to traditional accounting

Revenue timing is the biggest difference. A traditional company sells a product and recognizes revenue when control transfers. A SaaS company sells a 12-month subscription and usually recognizes revenue monthly over the contract term.

Additionally, cash doesn’t equal revenue. If a SaaS company collects $120,000 in January for annual contracts, it might only recognize $10,000 per month. The rest sits on the balance sheet as deferred revenue (a liability).

Recurring complexity is another differentiator. While traditional businesses rarely deal with mid-contract upgrades, seat expansions, downgrades, usage overages, pause requests, or free-trial conversions, SaaS companies handle these constantly.

The TL;DR: the SaaS financial model needs a different accounting setup to regular businesses because it uniquely involves tracking contracts over time, applying revenue rules consistently, and connecting subscription billing activity to accurate financial reporting. For a detailed breakdown of how each statement works for SaaS companies, see our SaaS financial statements guide.

ASC 606 revenue recognition for SaaS companies

ASC 606 is the revenue recognition standard ² that governs how SaaS companies record revenue. As outlined in our ASC 606 deep dive, it’s a five-step process: identify the contract, identify performance obligations, determine the transaction price, allocate the price, and recognize revenue as obligations are satisfied. For SaaS, this typically means recognizing subscription revenue ratably over the contract term.

The 5-step ASC 606 model (with SaaS examples)

- Identify the contract: A signed subscription agreement, order form, or enforceable click-through terms.

- Identify performance obligations: Usually access to the platform over time. Implementation or premium support may be separate obligations.

- Determine the transaction price: Total contract value including fixed fees, discounts, and estimated variable consideration. Example: $120K annual contract + $20K implementation = $140K.

- Allocate the price: If multiple obligations exist, allocate based on standalone selling prices. This is where bundled deals often create issues.

- Recognize revenue: Subscription revenue is typically recognized monthly over the term.³ Implementation may be recognized at a point in time or over time depending on the service.

Where SaaS companies get ASC 606 wrong

The most common mistake is recognizing annual contracts upfront. If $120K’s collected on January 1, you don’t have $120K of Q1 revenue. You actually have $30K of Q1 revenue and $90K of deferred revenue.

Another issue is not separating performance obligations. If software, onboarding, and premium support are bundled together, you can’t recognize it all as subscription revenue. Each part needs separate treatment.

Variable consideration is also often missed. Usage-based pricing, SLA credits, and tiered volume pricing all affect transaction price and may need estimates under ASC 606. ⁴

Deferred revenue: a challenge for the SaaS balance sheet

Deferred revenue is cash your SaaS company has collected for services you haven’t yet delivered. It sits on the balance sheet as a liability – not as revenue on the income statement – until the service period is fulfilled. For SaaS companies with annual or multi-year contracts, deferred revenue⁵ can represent millions in obligations.

How deferred revenue works: an example journal entry

Why deferred revenue matters beyond compliance

Deferred revenue misstatements are the #1 problem area in SaaS audits. If balances are wrong, this can majorly slow down fundraising, M&A, and IPO processes.

It also changes how performance is interpreted. A company might collect $5M in annual contract cash during a quarter while recognizing only a portion of that as GAAP revenue. Boards and investors need visibility into both, especially when reviewing the cash flow statement alongside the income statement.

It can also signal churn early. If deferred revenue ⁵ declines unexpectedly, future recognized revenue may weaken before it shows up elsewhere.

In short: for many SaaS companies, deferred revenue is one of the most important balance sheet accounts. Getting it right is essential.

For the full ASC 606 treatment — multi-element contracts, SSP allocation, and variable consideration — see our deferred revenue recognition practitioner's guide.

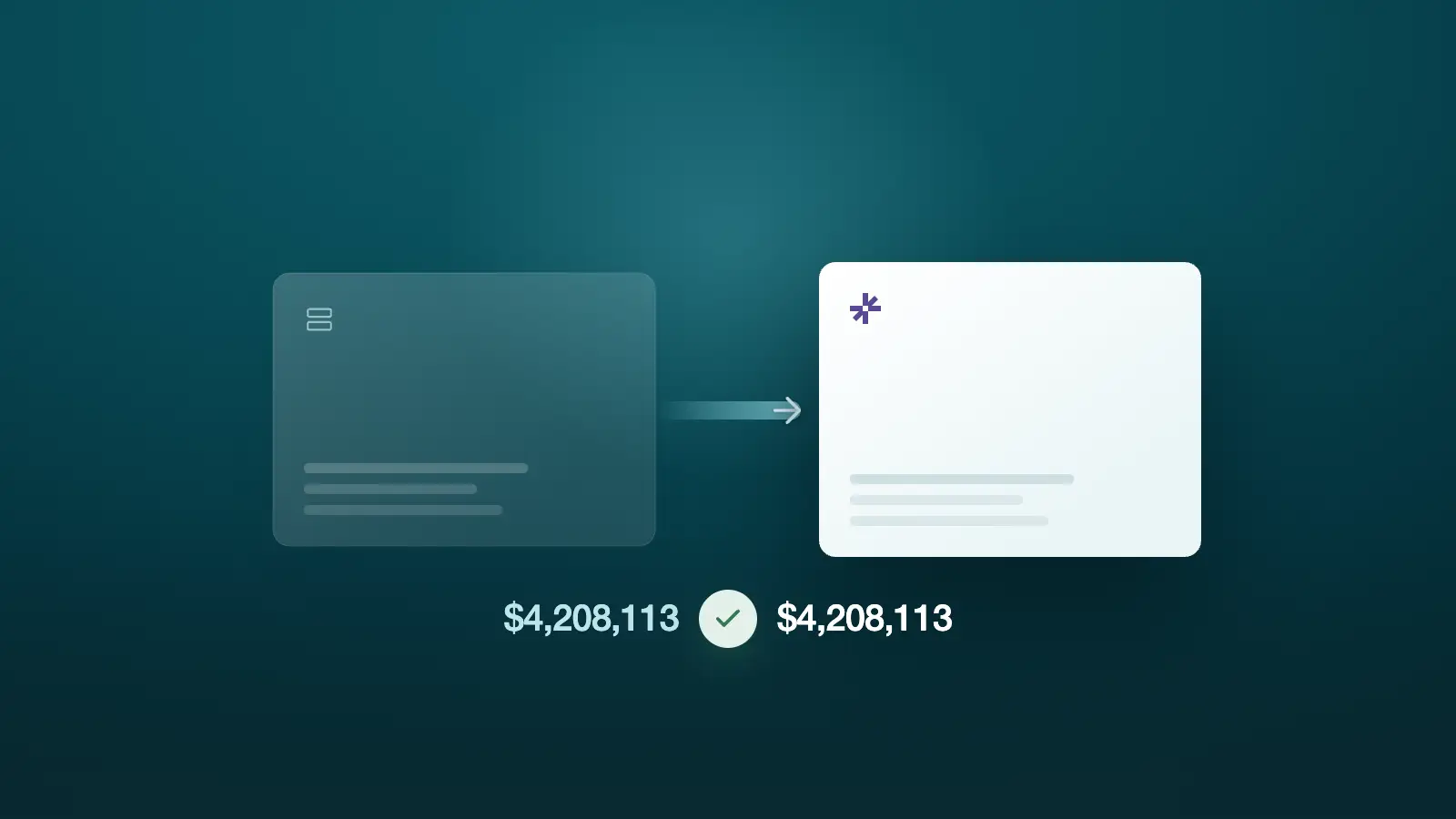

Bookings vs. billings vs. revenue – the SaaS accounting triangle

Bookings, billings, and revenue are often mixed up by SaaS companies. Bookings are the total contract value when a deal is signed. Billings are invoices sent to the customer. Revenue is what you’ve actually earned under ASC 606. A single $120K annual contract creates $120K in bookings on day one, $120K in billings, but only $10K in monthly revenue.

Here’s how one contract might flow through financials:

Understanding the relationship between all three metrics ⁶ is essential for clean reporting.

Investors ask for ARR… but not always the same ARR. Some want forward-looking bookings-based ARR; others care about recognized revenue ARR for GAAP-compliance purposes. So if teams use these terms loosely, due diligence gets harder.

These figures also affect cash planning. A company with $5M bookings, $3M billings, and $1M recognized revenue has very different cash needs than those numbers might suggest at first glance.

The SaaS accounting metrics that matter

The SaaS metrics that matter ⁷ for accounting are different from the ones your marketing team tracks. Finance teams need GAAP revenue, deferred revenue balance, net revenue retention, and gross margin, not just MRR and logo churn. Here’s a rundown of the metrics that belong in your SaaS accounting toolkit.

Key SaaS financial metrics

- MRR / ARR: Monthly and annual recurring revenue – a.k.a. the foundation of SaaS accounting. MRR is the total monthly subscription revenue from active contracts. ARR is MRR x 12. Calculate from recognized revenue, not bookings.

- Deferred revenue balance: Total cash collected for services not yet delivered. A growing deferred revenue balance (when paired with growing bookings) is a positive indicator. Declining deferred revenue without proportional churn is a warning sign.

- Net revenue retention (NRR): Revenue from the same customer cohort including expansion and contraction. Getting this to over 100% means you’re growing without acquiring new customers. The best SaaS companies hit around 120-140% NRR.

- Gross margin: Revenue minus the cost of goods sold (hosting, support, customer success). SaaS companies should target 70-85% gross margins. Below 65% raises questions during fundraising.

- CAC payback period: Time needed to recover customer acquisition cost (often assessed alongside customer lifetime value)using gross-margin-adjusted recurring revenue. For best-in-class SaaS companies, it should be under 18 months. Pair CAC payback with your cost structure to model your break-even point and see how pricing or cost changes shift the timeline.

For how to present these to your board, see how to build a SaaS metrics dashboard.

The Rule of 40 (and why accountants care about it)

The Rule of 40 ⁸ says revenue growth rate plus profit margin should equal or exceed 40%.

It’s important for finance teams because both inputs depend on accurate accounting. If revenue is overstated or margins are misclassified, the Rule of 40 becomes meaningless. Many investor narratives break down because the underlying numbers were weak. For a deep dive into OCF vs. FCF vs. Rule of 40 FCF margin — with ARR-stage benchmarks — see our SaaS cash flow analysis.

SaaS accounting by company stage

What your SaaS company needs from its accounting function changes dramatically as you scale. For example, a pre-revenue startup tracking burn rate in a spreadsheet has different needs to a $20M ARR company preparing for an audit. Here’s what to prioritize at each stage.

The biggest mistake is waiting too long. Companies often postpone cleanup until a fundraise or acquisition, then pay heavily for catch-up work.

When to upgrade from QuickBooks? Many SaaS teams hit an inflection point around $3M-$5M ARR, when spreadsheets and basic systems stop keeping up. At this stage, you’ll want to start evaluating QuickBooks replacements. More comprehensive platforms like DualEntry become more valuable for handling deferred revenue tracking, multi-entity complexity, and audit readiness. For a broader framework, see our guide on when tech SaaS startups need a full ERP.

If your startup is VC-funded, you'll also need to manage equity instrument accounting at each stage — see our VC-backed startup accounting requirements guide.

Common SaaS accounting mistakes

The most common SaaS accounting mistakes involve revenue recognition timing, metric miscalculation, and inadequate tooling. These aren’t theoretical risks – they cause audit failures, fundraising delays, and financial restatements.

Typical missteps:

- Recognizing annual contract revenue upfront: If you’re booking $120K as Q1 revenue when only $30k has been earned, this inflates revenue and understates liabilities. Auditors won’t be happy.

- Mixing cash-basis and accrual reporting: The numbers won’t line up – and your credibility will drop – if you use cash-basis reporting for internal dashboards while submitting accrual-basis financial statements to investors.

- Ignoring commission capitalization (ASC 340-40) ⁹: Sales commissions on contracts >12 months must be capitalized and amortized over the expected customer life, not expensed immediately. Most SaaS companies with under $10M ARR get this wrong.

- Not separating services revenue: Onboarding and implementation can distort SaaS margins if blended incorrectly. They should be handled individually.

- Tracking MRR from bookings instead of recognized revenue: Signed contracts are not the same as earned recurring revenue.

- Waiting too long to implement the right tools: Manual spreadsheet revenue schedules work until your company starts to scale. Switching sooner rather than later is wise – because the cost of retrospective restatement (not only financially) far exceeds the cost of migrating to proper SaaS accounting software at the right time.

Choosing the right SaaS accounting software

The best SaaS accounting software depends on your company stage and complexity. Early-stage startups can manage with QuickBooks or Xero plus spreadsheets. Scaling SaaS companies ($5M-$50M ARR) need automated revenue recognition, multi-entity support, and AI-driven workflows – which is exactly what DualEntry was built for.

Quick comparison: SaaS accounting software

What to look for in SaaS accounting software

- ASC 606 revenue recognition automation: Manual rev rec in spreadsheets breaks at 50+ contracts. Your software should be able to handle ratable recognition, usage-based billing, and multi-element arrangements automatically.

- Deferred revenue management: Real-time deferred revenue balance tracking, not month-end manual calculations.

- Multi-entity consolidation: If you have (or plan to have) international subsidiaries, you need automated intercompany elimination and multi-currency support.

- SaaS metrics built in: MRR, ARR, NRR, churn, and CAC payback should be calculated from your accounting data, not from a separate BI tool that may use different definitions.

- Audit readiness: Aim for clean audit trails, role-based access controls, automated reconciliation, and customizable, board-ready financial reporting.

Why DualEntry for scaling SaaS companies?

DualEntry is built for the gap between entry-level tools and heavyweight ERP implementations.

It combines AI-native workflows with core finance controls: automated revenue recognition, cash matching, AP automation, month-end close support, and multi-entity reporting.

For SaaS companies that are too complex for QuickBooks but not ready for expensive legacy ERP rollouts, it fits the growth-stage operating model.

It’s newer than long-established enterprise platforms, so companies with deep manufacturing or supply-chain needs may want to evaluate broader SaaS ERP suites as well.

See DualEntry’s plans and pricing to cover different enterprise needs.

The bottom line: getting SaaS accounting right

SaaS accounting is not regular accounting with subscriptions added on top. It’s a different discipline that revolves around timing, recurring contracts, and revenue earned over time.

To do it well, companies need strong ASC 606 processes, accurate deferred revenue tracking, and metrics grounded in real financial data.

Early-stage teams can start simple. Once growth accelerates, though, manual work gets riskier and more expensive. At this point, automation can be a game-changer, especially for companies managing multiple entities, larger contract volumes, and audit readiness.

DualEntry is designed for that exact transition. You can read more about its SaaS accounting features here, or check out our blog post on SaaS revenue recognition. If you’re ready to future-proof your finance setup as your business grows, schedule a demo to see how DualEntry can support.

SaaS Accounting FAQs

See the full power of DualEntry in 30 minutes

Woosung Chun

CFO, DualEntry

Woosung Chun is the CFO of DualEntry with experience in corporate finance, accounting, strategy, and acquisitions. He previously grew from scratch and led the M&A and Finance teams at Benitago, where he completed more than 12 acquisitions in 2 years. He graduated with a BS from NYU Stern. At DualEntry, Woosung writes about AI in accounting, revenue recognition, foreign currency accounting, hedge accounting, and ERP modernization for finance teams navigating complex, multi-entity environments.