Don't worry! The contents here will appear on the published page.

Citibank Revlon Wire Transfer Mistake: A Forensic Breakdown for Finance Leaders

Hugh Mitton

Video Producer, DualEntry

Hugh Mitton

Video Producer, DualEntry

Hugh Mitton is the Founding Video Producer at DualEntry, where he investigates the workflows, failures, and decisions shaping how finance teams operate — and translates original video reporting into long-form analysis for practitioners. This article grew from a video he produced on the Citibank/Revlon incident. Before DualEntry, he spent five years producing financial content for Fitch Group and built a documentary track record at Bleacher Report, where his work earned 15M+ organic views and coverage in TIME, BBC, CNN, and The Guardian.

Learn about our editorial policies.

Last updated

May 29, 2026

Reviewed by

Woosung Chun

.jpg)

Woosung Chun

CFO, DualEntry

Woosung Chun is the CFO of DualEntry with experience in corporate finance, accounting, strategy, and acquisitions. He previously grew from scratch and led the M&A and Finance teams at Benitago, where he completed more than 12 acquisitions in 2 years. He graduated with a BS from NYU Stern. At DualEntry, Woosung writes about AI in accounting, revenue recognition, foreign currency accounting, hedge accounting, and ERP modernization for finance teams navigating complex, multi-entity environments.

Learn about our editorial policies.

Summarize this article

On August 11, 2020, three trained professionals processed what should have been a $7.8 million interest payment. By end of day, $894 million had left Citibank's accounts and landed in the hands of Revlon's creditors.

Nobody was hacked. No insider threat. The cause of the Citibank Revlon wire transfer mistake was a checkbox, left unchecked, in a legacy banking platform that silently reverted to its default behavior when the configuration was incomplete. The software did exactly what it was designed to do. That was the problem.

The incident has been covered from every angle except the one that matters most to finance leaders. Lawyers analyzed the discharge for value doctrine. UX writers blamed bad interface design. The financial press focused on the $400 million OCC fine. Nobody has asked the question that should matter more: does the same failure pattern exist in your payment workflows right now?

For most finance teams running on enterprise software built for different workflows, the honest answer is that the conditions are already there. The incident just hasn't happened yet.

This is a forensic breakdown of what went wrong, and a practical audit for finance leaders who want to make sure it doesn't happen to them.

If you prefer video, here's the full breakdown:

What actually happened: the four phases of a $900M error

Citibank's $894 million wire transfer mistake unfolded in four distinct phases: a software workaround that created the conditions for error, a review chain that amplified rather than caught it, an overnight discovery, and a multi-year legal battle over whether the recipients were legally required to return the funds.

Phase 1: The software workaround nobody questioned

Oracle Flexcube, Citibank's enterprise banking platform, wasn't built for the specific transaction the team needed to execute. Citibank served as administrative agent on a $1.8 billion syndicated loan facility for Revlon. The goal was routine: send a $7.8 million interest payment to creditors while redirecting the principal to an internal wash account.

Flexcube couldn't do that natively. So the team used a workaround: check three boxes labeled "Front," "Fund," and "Principal" to route funds appropriately. What nobody formally documented, trained on, or risk-assessed was what happened when those boxes were left unchecked. The answer: Flexcube reverted silently to its default. Send everything.

On August 11, 2020, the operator checked only the "Principal" box. The other two were left unchecked. The system didn't flag an error. The final confirmation popup said only that "funds will be sent out of the bank," with no recipient, no amount, no context. From the software's perspective, it was working exactly as designed.

$894 million went out.

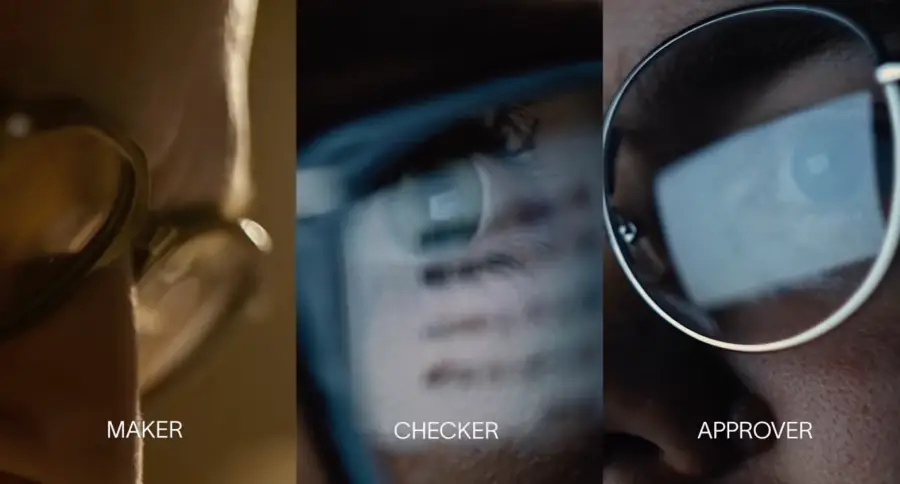

Phase 2: Why three reviewers all made the same mistake

Citibank's six-eyes protocol required three independent reviewers: a maker, a checker, and an approver. The assumption built into this structure is that independent reviewers catch different errors. What the behavioral economics research on anchoring shows is that sequential review often does the opposite. [6]

When the first reviewer approves a transaction, each subsequent reviewer anchors to that judgment. They're no longer examining the transaction independently. They're validating a prior decision. It's not negligence. It's how human cognition works under conditions of uncertainty with limited information.

All three reviewers believed the principal would "wash" to the internal account. That phrase appeared in the approver's sign-off email: "Looks good, please proceed. Principal is going to wash." All three made the same logical inference from the same incomplete information, in sequence, each reinforcing the last. None knew the checkbox rule: unchecked boxes don't hold, they default.

Table 1: The six-eyes failure pattern

Phase 3: Discovery, recall, and the $385M that was returned

The morning reconciliation on August 12 revealed the error within hours. Citibank's initial suspicion was a Flexcube bug. By afternoon, the team had confirmed a human configuration error and began issuing recall notices to 315 lenders across the syndicate.

Most returned the funds. Approximately $385 million was voluntarily returned. Ten investment firms, including Brigade Capital and HPS Investment Partners, refused. Their argument: they were legitimate creditors, the amount matched the outstanding debt, and under New York's discharge for value rule, they had no legal obligation to give it back.

By that point, Revlon's debt was trading at roughly 20 cents on the dollar. The lenders knew exactly what they were holding.

Phase 4: The legal battle and what changed afterward

In February 2021, a US District Court judge sided with the lenders. The amount matched the debt "to the penny." That was enough to invoke discharge for value protection. Citibank appealed. [1]

In September 2022, the Second Circuit reversed. Because the loan wasn't due for three more years, the lenders were on "inquiry notice" that the payment was a mistake. They couldn't claim ignorance of an error they had reason to suspect. [2]

Citibank recovered the funds, but the broader damage had already landed. The OCC had issued a $400 million fine in October 2020 for "longstanding deficiencies" in risk management and data governance. [3] Revlon, caught in the legal crossfire and already in financial distress, filed for bankruptcy in 2022. The industry response was a new contractual clause added to syndicated loan form agreements: the erroneous payment provision, now widely called the Revlon Blocker. [4]

The real lesson: your ERP is part of your internal control framework

Most finance leaders treat their ERP or payment software as a workflow tool. The Citibank incident establishes something different: enterprise software design is internal controls infrastructure. When software encourages workarounds, creates ambiguous confirmation flows, or silently reverts to dangerous defaults, it creates documented control deficiencies regardless of how many human reviewers are in the chain.

The Flexcube checkbox failure wasn't a UX problem. It was a COSO problem. And the COSO framework is the language your auditors, your board, and your CFO liability speak.

The COSO framework lens: where Flexcube failed

The COSO Internal Control Framework identifies five components of effective internal control: Control Environment, Risk Assessment, Control Activities, Information & Communication, and Monitoring. [5] Flexcube's design violated at least three of these simultaneously. That's not a one-time user error. That's a systemic control failure.

Table 2: COSO control failure mapping

The distinction that matters here: COSO doesn't care whether the failure was human or software. It cares whether the control existed and whether it worked. A confirmation popup that shows no amounts isn't a control. It's theater.

The workaround problem: when software becomes a liability

Here's what the Citibank post-mortems almost universally missed: the Flexcube checkbox workaround wasn't a Citibank problem. It was a software-workflow mismatch problem. And software-workflow mismatches produce workarounds in every finance team, at every company, at every stage.

When your ERP can't natively handle a transaction your business regularly executes, someone builds a workaround. They show it to the team. The team uses it. Nobody writes it down, nobody risk-rates it, nobody puts it in a control narrative. It lives in institutional memory. Then someone new joins the team, or someone misremembers the steps, and the workaround fails in a direction the software was never designed to catch.

The Flexcube workaround was operational for years before August 2020. It never appeared in an audit because it was never formally documented. It was a latent risk existing entirely outside the auditable control environment, waiting for a single unchecked box.

The question for your organization isn't whether this pattern exists. It does. The question is: what are the workarounds in your payment and close processes right now, and what happens when one of them fails?

What to do differently: a payment controls audit for finance leaders

The Citibank incident maps to five questions every finance leader can ask about their own operations. You don't need to be running a billion-dollar syndicated facility for these to apply. If your team processes wires, runs multi-person approval chains, or relies on ERP software to enforce controls at execution, these failure modes are relevant.

Table 3: Payment controls self-audit

Question four is the one most teams will struggle with. Not because the workarounds don't exist, but because nobody has ever asked that question before.

What is the Revlon Blocker, and does your debt agreement have it?

The erroneous payment provision, called the Revlon Blocker after the 2020 incident, is a contractual clause that requires lenders to return any payment they receive from an administrative agent that was made in error. Even if the amount matches outstanding debt. Even if the funds have already been deployed.

It emerged from Loan Syndications and Trading Association (LSTA) form agreement updates in late 2020 and 2021, triggered by the District Court ruling that initially let the lenders keep Citibank's money. The Second Circuit eventually reversed that ruling, but the industry had already moved to close the gap contractually.

If your company carries syndicated debt, your loan agreement should include this clause. If it was executed before 2021 on a standard template, there's a reasonable chance it doesn't. That's worth a conversation with your legal team.

If your company acts as an administrative agent on any credit facility, this clause is critical to your operational risk profile. Full stop.

The broader pattern: why legacy financial software is a risk event

The Revlon incident wasn't a one-off. It was a visibility event — the moment a failure pattern that exists across the industry became impossible to ignore. Operations teams at institutions of every size are running mission-critical processes on software designed for different workflows, extended with undocumented workarounds, and approved by review chains that create false confidence rather than genuine oversight.

The failure anatomy is consistent. The amounts are different. The mechanics are the same.

Table 4: The anatomy of a software-driven financial controls failure

The last row is worth pausing on. When something goes wrong in a finance process, the instinct is to find the person who made the error. That instinct produces retraining, disciplinary reviews, and checklists. It rarely produces an honest audit of whether the software itself created the conditions for failure.

For mid-market finance teams, the workflow mismatch problem is acute. Platforms built for earlier stages or different business models get extended with spreadsheet bridges, manual journal entries, and offline approval chains that nobody has formally risk-assessed. The pattern isn't the scale. It's the structure: software that doesn't fit the workflow, extended informally, reviewed by teams who don't fully understand the underlying system logic. [INTERNAL LINK: ERP for SaaS]

DualEntry was built for that gap specifically. AI-native accounting infrastructure designed for mid-market SaaS finance teams, where the workflow is the software rather than the workaround. That doesn't mean the failure pattern disappears. It means the surface area shrinks considerably.

The checkbox was the symptom, not the disease

Citibank didn't lose $894 million because an employee checked the wrong box. They lost it because the software was designed to make the right action hard and the catastrophic default invisible.

The checkbox was the symptom. The disease was treating software as a neutral workflow tool rather than a component of the financial control environment.

The $400 million OCC fine wasn't for the Revlon wire. It was for "longstanding deficiencies" in risk management and data governance. Revlon was the visible crisis of an invisible systemic failure the OCC had been documenting for years. And the industry's response — a contract clause, not a software redesign — tells you something about where the incentives point.

For finance leaders, the question isn't whether you use legacy software. Most do. The question is whether you've mapped your software's failure modes to your control framework, and whether you have a plan to close the gaps.

Finance operations runs on software. The only real question is whether that software is designed to make errors obvious or invisible.

Book a demo to see how DualEntry approaches financial controls differently.

Citibank Revlon Wire Transfer Mistake FAQ

See the full power of DualEntry in 30 minutes

Hugh Mitton

Video Producer, DualEntry

Hugh Mitton is the Founding Video Producer at DualEntry, where he investigates the workflows, failures, and decisions shaping how finance teams operate — and translates original video reporting into long-form analysis for practitioners. This article grew from a video he produced on the Citibank/Revlon incident. Before DualEntry, he spent five years producing financial content for Fitch Group and built a documentary track record at Bleacher Report, where his work earned 15M+ organic views and coverage in TIME, BBC, CNN, and The Guardian.