Don't worry! The contents here will appear on the published page.

Accounting for Venture-Backed Startups: The Complete Stage-by-Stage Guide (2026)

Woosung Chun

CFO, DualEntry

.jpg)

Woosung Chun

CFO, DualEntry

Woosung Chun is the CFO of DualEntry with experience in corporate finance, accounting, strategy, and acquisitions. He previously grew from scratch and led the M&A and Finance teams at Benitago, where he completed more than 12 acquisitions in 2 years. He graduated with a BS from NYU Stern. At DualEntry, Woosung writes about AI in accounting, revenue recognition, foreign currency accounting, hedge accounting, and ERP modernization for finance teams navigating complex, multi-entity environments.

Learn about our editorial policies.

Last updated

July 2, 2026

Reviewed by

Do San (Justin) Myung

Do San (Justin) Myung

Expert Accountant & Former Consulting CFO | DualEntry

Justin (Do San Myung) is Expert Accountant at DualEntry with 20+ years of hands-on experience managing general ledgers, financial close processes, and ERP implementations for mid-market and enterprise companies. As a former Consulting CFO and Controller, he has personally overseen month-end closes, SOX compliance programs, and multi-entity consolidations across technology, manufacturing, and services industries. Justin specializes in transforming manual accounting workflows into automated, AI-driven processes.

Learn about our editorial policies.

Summarize this article

Your $2M wire just cleared. Product and hiring are already pulling your attention, and accounting feels like something to sort out later. The hard truth? “Later” is where it gets expensive.

Founders who push accounting for startups down their priority list through seed stage routinely spend $55,000 to $145,000 cleaning the books up before their Series A. Restated financials, reclassified equity instruments, missing stock comp expense… auditors will find all of it.

This guide walks through what venture-backed startup accounting actually calls for at each stage: from infrastructure to VC-specific needs. If you're newer to SaaS accounting fundamentals — accrual basis, ASC 606, and the SaaS-specific general ledger structure — read that guide first before diving into the VC-specific layer.

What makes venture-backed startup accounting different

Venture-backed startup accounting differs from standard small-business accounting in three core ways: the presence of equity instruments (SAFEs, options, warrants), the obligation to produce investor-grade financial reporting, and a trajectory toward GAAP-audited financials that most small businesses never need.

SMB vs. venture-backed startup accounting

Each funding event leaves an instrument on your balance sheet that needs its own accounting treatment. SAFEs, convertible notes, stock options, and warrants are covered by different standards and don't behave the same way. Your investors then want monthly financials with actuals vs. budget and SaaS metrics, not a year-end summary. By Series A, investors need audited GAAP financials – so the books you kept at seed must be audit-ready.

Starter accounting tools (think QuickBooks and Xero) work out of the box for an SMB. For a venture-backed startup, however, a “default” chart of accounts from those platforms isn't enough to handle ASC 606[10] deferred revenue, equity classes, or stock comp, so at this point it's time to start looking for more powerful accounting software built for multi-entity reporting, automated revenue recognition, and audit-ready financials.

The Stage-Gate Framework: What Changes at Each Funding Milestone

Accounting needs for venture-backed startups aren't static – they escalate at each funding milestone. Pre-seed demands basic accrual bookkeeping. Seed introduces equity accounting and investor reporting. Series A triggers GAAP-compliant financials. Series B requires consolidated reporting and full FP&A infrastructure.

Stage-gate accounting needs

Pay attention to the transitions between rows. The jump from pre-seed to seed startup bookkeeping is where SAFEs start to build up, and your first 409A comes in. The shift from seed to Series A is where founders often get hurt. At this stage, informal monthly reporting is replaced by audit-ready GAAP financials, and any gaps from earlier periods start to appear during diligence.

By the time you've signed a Series A term sheet, your books should already be organized according to Series A accounting requirements. Auditors review what's on file today, regardless of which stage you were at when each entry was posted.

Equity Instruments in Accounting for VC-Backed Startups

Venture-backed startup accounting introduces equity instrument complexity that bootstrapped companies never face. SAFEs and convertible notes need classification under ASC 480,[2] stock option grants create ongoing non-cash expense under ASC 718,[5] and every option issuance requires a current 409A valuation. Founders who skip this infrastructure face $55,000–$145,000 in retroactive cleanup costs at Series A.[1]

How to account for SAFE notes and convertible notes

SAFEs and convertible notes are among the most frequently misclassified instruments in early-stage startup accounting. Under ASC 480[2] (and ASC 815-40[3]), a SAFE's classification depends on its specific terms. SAFEs do not convert at the company's option — they convert automatically upon a qualifying financing round. A discount-only SAFE may require liability classification under ASC 480-10-25-14(a)[2] due to the fixed monetary value of settlement; a cap-only SAFE is analyzed under ASC 815-40;[3] a SAFE with both a discount and cap requires a predominance assessment. Convertible notes are recorded as debt with interest accrual until they convert at a qualifying financing round.

SAFEs are among the most frequently misclassified instruments in early-stage startups. They're often booked as revenue or just ignored by founders (until an auditor comes looking).

The correct journal entry at close is straightforward: debit cash, credit APIC – SAFE Instrument.

But you still need the ASC 480[2] memo on file documenting the equity classification. YC introduced the post-money SAFE in September 2018.[4] Classification as equity is common in practice, but requires a completed analysis under ASC 480[2] and ASC 815-40[3] — many SAFEs may require liability classification depending on their specific terms. The ASC 480 memo is what gets you through audit scrutiny.

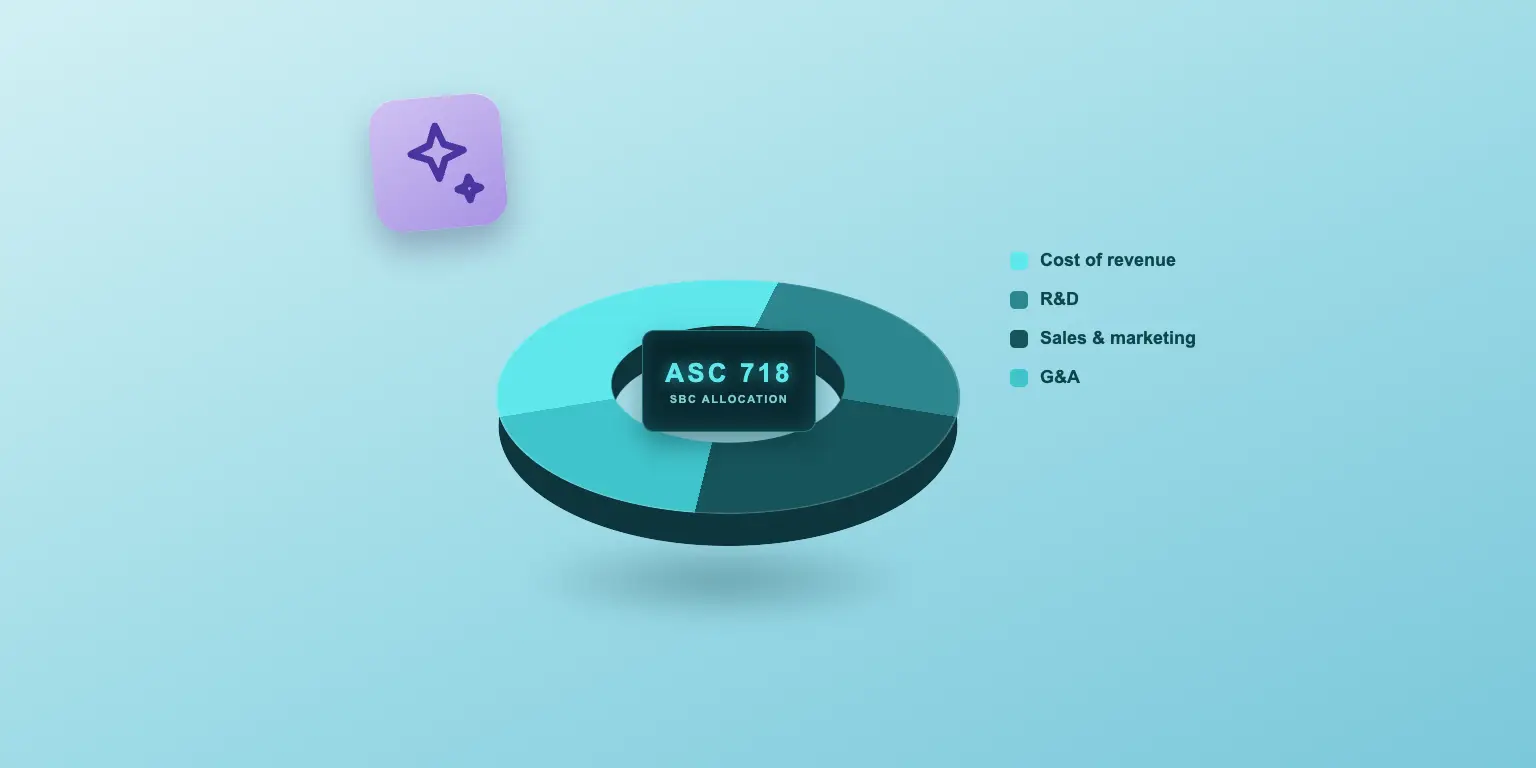

Stock-Option Expense: ASC 718 Basics

Every stock option grant creates a non-cash compensation expense that must be recognized over the vesting period under ASC 718.[5] Fair value is calculated at grant date using the Black-Scholes model,[6] with the 409A valuation setting the exercise price floor. For cliff-vesting grants, monthly expense equals total grant fair value divided by total vesting months. For graded-vesting schedules, each tranche is expensed separately over its own vesting period, producing higher expense in early periods – and must be recorded whether or not cash changes hands.

The exercise price is both a legal point and an accounting input. A current 409A is what makes that price defensible at fair market value, and the Black-Scholes[6] calculation builds on it with the exercise price, time to expiry, risk-free rate, and volatility.

If you don't record your ASC 718[5] expense, you face financial restatement risk, problematic audit findings, and a drop in investor trust.

When Do You Need a 409A Valuation?

A 409A valuation is an IRS-required independent appraisal of a startup's common stock fair market value, mandatory before issuing any employee stock options.[7] Without a current 409A, option grants are treated as deferred compensation under IRC Section 409A – making them immediately taxable and subject to a 20% excise tax penalty[8] for every employee who received options at an improper price.

Get one before your first option grant, refresh it after every priced round – and refresh it again after any material event. You can expect the costs to be $1,000–$5,000 at early stage and $2,500–$10,000+ by Series B[9] (higher for complex cap tables or pre-IPO situations). Carta and Pulley are among the most widely used providers; Aranca and Preferred Return also offer 409A services.

The Series A Audit Trap and the Cost of Bad Early Books

Startups that defer proper accounting through pre-seed and seed stage routinely face $55,000–$145,000[1] in retroactive cleanup costs when Series A investors request GAAP-compliant audited financials. Costs include restating financial statements, reclassifying equity instruments, recording omitted stock comp expense, and paying auditors to work through incomplete records.

Series A cleanup cost model

Building the Best Accounting Stack for Your Company Stage

The right accounting stack for a venture-backed startup scales with funding stage and headcount. Pre-revenue can run on QuickBooks and a part-time bookkeeper. Seed stage adds cap table software and a fractional CFO. Series A needs a controller or accounting firm with audit experience, cap table software reconciled to the GL, and FP&A tooling for board reporting.

What accounting software should a startup use?

Recommended accounting stack by stage

The Series A row is where most founders hit a wall. QuickBooks and Xero start to show cracks when you're faced with audit-grade demands – but the reality is, at that stage you're also 2+ funding rounds away from hiring a full internal accounting team. This is where accounting ERPs like DualEntry and NetSuite come in, offering the level of audit-ready GAAP accounting and reporting depth your Series A lead will expect.

For a deeper comparison of which platforms work at each stage, see our guide to the best ERP system for tech startups.

What Investors Expect: The Monthly Reporting Package

After closing a funding round, VC investors expect a standardized monthly reporting package: a P&L with actuals vs. budget, balance sheet, cash flow statement, and key SaaS metrics – including ARR (annual recurring revenue) and MRR (monthly recurring revenue), plus NRR, GRR, CAC, and LTV. Consistently accurate reporting is foundational to investor confidence — errors that compound across multiple reporting periods are difficult to walk back even when product traction is strong.

What financial reports do VCs expect from portfolio companies?

A standard board package checklist

- Income statement (P&L): Actuals vs. budget; current month + YTD

- Balance sheet: Current month vs. prior month

- Cash flow statement: Operating; investing; financing activities

- Runway calculation: Months of cash left at current net burn rate

- ARR / MRR bridge: With new, expansion, contraction, and churn broken out separately

- NRR and GRR: Reconciled to GAAP revenue (not cash receipts)

- CAC and LTV by cohort, if available

- Headcount and hiring plan vs. actual

For the precise formulas and stage-appropriate benchmarks investors will compare you against, see our guide to SaaS unit economics benchmarks.

Conclusion

The smartest startups build a proper accounting setup at the seed stage. The initial cost is worth it when the alternative is a six-figure correction at Series A.

DualEntry is built for the Series A inflection point, where starter accounting setups like QuickBooks stop scaling with you but you'd rather keep running lean than adding to your Finance headcount. Schedule a demo to see how DualEntry handles the accounting complexity VC-backed startups face, helping you achieve more in less time.

Venture backed startup accounting FAQs

See the full power of DualEntry in 30 minutes

Woosung Chun

CFO, DualEntry

Woosung Chun is the CFO of DualEntry with experience in corporate finance, accounting, strategy, and acquisitions. He previously grew from scratch and led the M&A and Finance teams at Benitago, where he completed more than 12 acquisitions in 2 years. He graduated with a BS from NYU Stern. At DualEntry, Woosung writes about AI in accounting, revenue recognition, foreign currency accounting, hedge accounting, and ERP modernization for finance teams navigating complex, multi-entity environments.