Don't worry! The contents here will appear on the published page.

General Ledger Adjustments: Definition, Process & Examples

Do San (Justin) Myung

Expert Accountant & Former Consulting CFO | DualEntry

Do San (Justin) Myung

Expert Accountant & Former Consulting CFO | DualEntry

Justin (Do San Myung) is Expert Accountant at DualEntry with 20+ years of hands-on experience managing general ledgers, financial close processes, and ERP implementations for mid-market and enterprise companies. As a former Consulting CFO and Controller, he has personally overseen month-end closes, SOX compliance programs, and multi-entity consolidations across technology, manufacturing, and services industries. Justin specializes in transforming manual accounting workflows into automated, AI-driven processes.

Learn about our editorial policies.

Last updated

April 17, 2026

Reviewed by

Woosung Chun

.jpg)

Woosung Chun

CFO, DualEntry

Woosung Chun is the CFO of DualEntry with experience in corporate finance, accounting, strategy, and acquisitions. He previously grew from scratch and led the M&A and Finance teams at Benitago, where he completed more than 12 acquisitions in 2 years. He graduated with a BS from NYU Stern. At DualEntry, Woosung writes about AI in accounting, revenue recognition, foreign currency accounting, hedge accounting, and ERP modernization for finance teams navigating complex, multi-entity environments.

Learn about our editorial policies.

Summarize this article

Most of the numbers in your general ledger are recorded as transactions happen – but not all of them. Some need to be updated at the end of the period, which is where general ledger adjustments come in.

During the close process, finance teams use these adjustments to capture accruals, deferrals, corrections, and reclassifications. These entries bring the numbers into line before reporting.1

When handled properly, adjustments support a reliable trial balance and financial statements. Plus, they create the audit trail needed to stand up to external review.

In this article, we’ll cover what general ledger adjustments are, where they come from, the most common errors behind them, and a simple four-step framework to manage them – all with examples to make everything clear.

What is a general ledger adjustment?

A general ledger adjustment is the result of an adjusting journal entry recorded at the end of an accounting period.

These entries ensure revenues and expenses are recognized in the correct period under accrual accounting.2 They update account balances for accruals, deferrals, estimates, and corrections identified during close.

Note that these adjustments are different from routine postings: they happen after the initial, unadjusted trial balance is prepared, before financial statements are finalized. They need to be posted to the GL to make sure the adjusted trial balance reflects the updated account balances.3

What are these adjustments for?

General ledger adjustments ensure financial statements reflect the right activity in the right period.

They apply core accounting principles, aligning revenue and related expenses in the same reporting window – and aligning with GAAP and IFRS requirements that financial statements should reflect the conditions that existed at the reporting date.3

In most businesses, adjusting entries are required whenever financial statements are prepared, not just at year-end. Overlooking them can skew reporting.

Situations that often call for adjustments

Adjustments typically come up in the following scenarios:

- Deferrals: Prepaid expenses and unearned revenue need to be spread across the periods they relate to

- Accruals: Expenses or revenues that exist but haven’t been recorded yet (e.g. wages payable; earned revenue not invoiced)

- Estimates: Depreciation, bad debt provisions, and inventory adjustments based on judgment

- Reclassifications and corrections: Moving balances between accounts or fixing prior errors4

Common ledger errors

Ledger errors usually come from missing or misused information. Think omissions, incorrect postings, duplication, or the wrong accounting treatment being applied.

Transposition errors (when two digits or characters accidentally get swapped) also happen regularly, throwing the trial balance off with a difference that’s divisible by 9.5

What happens when these problems are left unresolved? They can distort profit, assets, liabilities, and equity. In more serious cases, they require formal correction and disclosure under accounting standards like IAS 8.6

Examples of ledger adjustments

Let’s look at some simple examples of slip-ups: first, a duplicated expense. Imagine a $3,000 invoice is recorded twice, so both Expenses and Liabilities end up overstated.

The adjustment goes as follows:

- Debit Accounts Payable $3,000

- Credit Expense $3,000

This removes the duplicate and restores the correct balance.

Another common case is a missing accrual. If $4,000 in wages has been incurred but not recorded, the adjusting entry should be:

- Debit Wage Expense $4,000

- Credit Wages Payable $4,000

This captures the obligation in the correct period and makes sure expenses are complete.

General ledger adjustments – step by step

Adjustments follow a structured process. The goal is to identify issues, correct them, and confirm the ledger reflects the right position before reporting.

Step 1: Identify the error

Start with reconciliations and account reviews. Compare ledger balances to external evidence like bank statements, supplier records, or physical counts.

Differences between subledgers (like AR or AP) and GL control accounts often point to missing or incorrect entries.7 If you review your trial balance regularly, this will help bring up any unusual movements or inconsistencies faster.

Step 2: Prepare the adjusting journal entry

Once the issue is clear, you need to figure out which accounts are affected and whether they need a debit or credit.

To support smooth audits and reporting, every adjusting entry should include:

- the date

- accounts

- amounts (debits and credits)

- a short explanation

Step 3: Post the adjustments

Adjusting entries are posted to the general ledger just like any other journal entry.

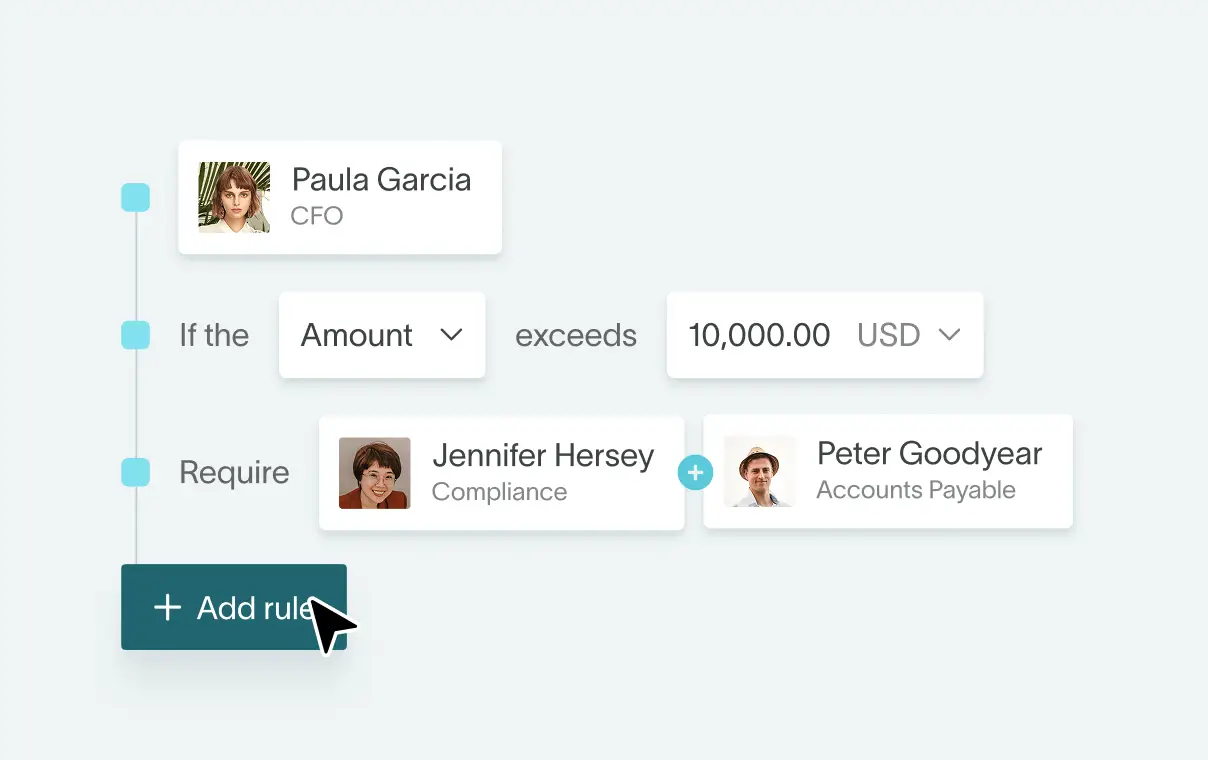

This triggers updates to the running balances in each GL account, then reflected in the adjusted trial balance. Because adjusting entries are considered as non-routine entries, for control reasons it’s recommended that a senior member of your finance team reviews or approves them.

Step 4: Validate with the trial balance and financial reports

After posting, prepare an adjusted trial balance to confirm that debits and credits match. Afterwards, you can go ahead and produce your financial statements.

How that adjustment format typically looks

Keeping financial statements accurate

General ledger adjustments turn a rough set of numbers into reliable financial statements. Without them, reports based on an unadjusted trial balance can miss accrued expenses, ignore earned revenue, or misclassify balances. That leads to incomplete or misleading results.

Adjustments, then, are important for filling in any gaps before reporting. Done right, they ensure that income statements reflect a period’s performance correctly and that balance sheets show the right position at the reporting date.

IFRS and GAAP say that material errors and omissions must be corrected – and that in some cases, prior periods should also be restated to keep the books consistent and transparent.

When audit time comes around, having a structured adjustment and review process (and clear documentation to back it up) will make everything smoother. So it’s worth taking time to get these foundations right.

How can AI automate general ledger adjustments?

AI and automation are changing how adjustments are identified and managed.

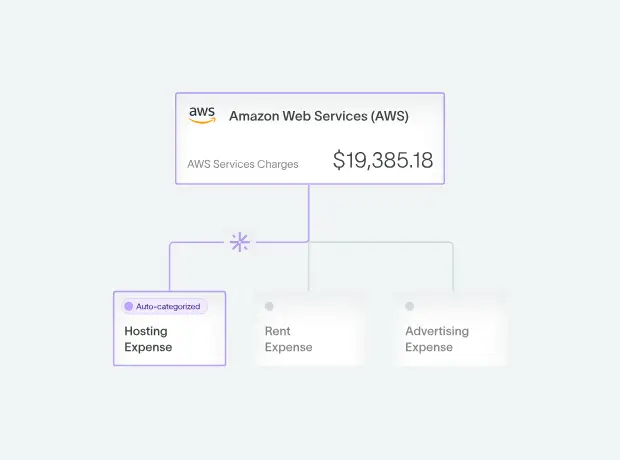

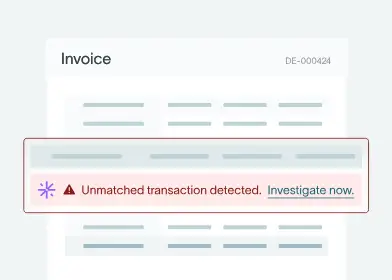

Putting tedious manual sample reviews in the past, AI-native software can scan entire ledgers in minutes and flag up unusual patterns, account combinations, or anything else that looks off and probably needs attention.

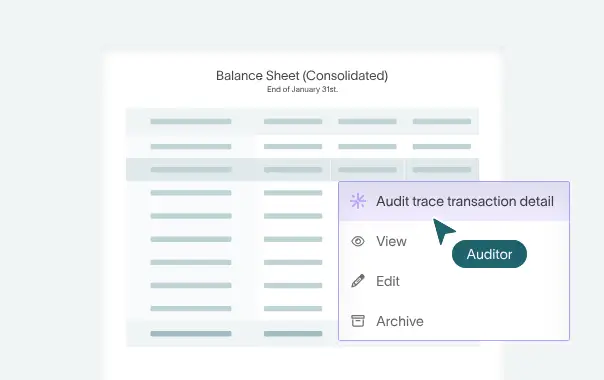

As every transaction is reviewed, not just a subset, errors have a lower chance of slipping through – and when they do, they come up earlier, so there’s no more last-minute surprises at close time. AI-native general ledger software like DualEntry build on this by combining anomaly detection with structured workflows, supported by real-time dashboards for a unified look into the close process. Audit trails get stronger, too, with GL adjustments documented automatically.

It’s important to note that AI isn’t replacing accountants. It instead frees them up to focus on strategic work, and supports a controlled, streamlined review and approval process.8

General Ledger Adjustments FAQs

Final thoughts

GL adjustments bridge the gap between financial statements and what actually happened during the reporting period. They apply accrual accounting principles so revenue and expenses are recorded at the right time.

Remember that a clear process helps: identify the issue, prepare the entry, post it, then validate the results. Combine this setup with strong documentation and regular, careful review, the whole process becomes reliable and easy to audit.

Handling adjustments manually works for a while when companies are small but, as soon as their transaction volumes increase, the process becomes hard to manage. Platforms like DualEntry take away these growing pains by automating recurring adjustments, flagging anomalies early, and keeping a structured record of every change – including who made it and when – with robust audit trails.

Overall, a disciplined approach supported by the right systems keeps your reporting accurate and defensible. To see how an AI-native ERP can make your entire GL accounting process faster, smoother, and more compliant as your business grows, schedule a demo.

See the full power of DualEntry in 30 minutes

Do San (Justin) Myung

Expert Accountant & Former Consulting CFO | DualEntry

Justin (Do San Myung) is Expert Accountant at DualEntry with 20+ years of hands-on experience managing general ledgers, financial close processes, and ERP implementations for mid-market and enterprise companies. As a former Consulting CFO and Controller, he has personally overseen month-end closes, SOX compliance programs, and multi-entity consolidations across technology, manufacturing, and services industries. Justin specializes in transforming manual accounting workflows into automated, AI-driven processes.

.webp)