Don't worry! The contents here will appear on the published page.

Handling Balance Sheet Reconciliation in the Automation Age

Do San (Justin) Myung

Expert Accountant & Former Consulting CFO | DualEntry

Do San (Justin) Myung

Expert Accountant & Former Consulting CFO | DualEntry

Justin (Do San Myung) is Expert Accountant at DualEntry with 20+ years of hands-on experience managing general ledgers, financial close processes, and ERP implementations for mid-market and enterprise companies. As a former Consulting CFO and Controller, he has personally overseen month-end closes, SOX compliance programs, and multi-entity consolidations across technology, manufacturing, and services industries. Justin specializes in transforming manual accounting workflows into automated, AI-driven processes.

Learn about our editorial policies.

Last updated

April 6, 2026

Reviewed by

Woosung Chun

.jpg)

Woosung Chun

CFO, DualEntry

Woosung Chun is the CFO of DualEntry with experience in corporate finance, accounting, strategy, and acquisitions. He previously grew from scratch and led the M&A and Finance teams at Benitago, where he completed more than 12 acquisitions in 2 years. He graduated with a BS from NYU Stern. At DualEntry, Woosung writes about AI in accounting, revenue recognition, foreign currency accounting, hedge accounting, and ERP modernization for finance teams navigating complex, multi-entity environments.

Learn about our editorial policies.

Summarize this article

Balance sheet reconciliation: it doesn’t sound exciting, but it’s one of the most important checks in accounting. Accuracy is everything when your financial statements are concerned, and reconciliation is what upholds this. Done properly, it confirms that balances are complete, correct, and evidence-backed before statements are finalized.1 Done badly, mistakes (and, sometimes, major control issues) can slip through – potentially leading to uncomfortable conversations with auditors and regulators in the future. So it’s essential to get this process right.

In this blog post, we look into what balance sheet reconciliation involves, why it matters, and how automation and AI can make it faster and easier to manage.

What it is – and why it’s important

Balance sheet reconciliation is the process of checking that the balances in your general ledger (GL) match the evidence behind them. That evidence might be bank statements, subledger reports, or detailed schedules that explain how each balance was calculated.

The goal here is simple: making sure assets, liabilities, and equity balances are complete, accurate, and recorded in the correct period, as part of the broader account reconciliation process. Accurate reconciliations help to make sure financial statements present a fair, reliable picture of a business, whether under GAAP2, IFRS3, or other reporting standards.

For auditors and regulators, reconciliation is a key internal control over financial reporting. It’s one of the main ways for companies to show that the numbers in their external filings and reports can be trusted.

Common examples include reconciling cash to bank statements, or matching accounts receivable (AR) and accounts payable (AP) balances to their aging reports. Any differences, like timing gaps or missing entries, have to be clearly explained and documented.4

Strong reconciliations rely on clear procedures, capable preparers, and timely completion. These are all emphasized in internal control frameworks like COSO.

The traditional reconciliation process, step by step

For most accounting teams, balance sheet reconciliations follow a fairly consistent process. Some of the steps below might change depending on a business’ size and financial complexity, but the aim is always to make sure every balance in the ledger is backed up with evidence.

- List the accounts that need reconciling

Start with a full list of balance sheet accounts. For each one, identify the supporting documents you’ll need – things like bank statements, subledger reports, contracts, or fixed-asset registers.5 - Compare the ledger to the supporting records

The preparer checks the GL balance against the independent source. Any differences should be flagged for deeper investigation. - Work out what caused the difference

Some issues are normal timing differences (e.g. transactions still in transit). Others are true errors (e.g. missing, duplicated, or misclassified entries). - Fix errors while the period is still open

If a discrepancy reflects an error or omission, a correcting journal entry needs to be posted so the financial statements reflect the right balance. - Get a final expert review

A knowledgeable reviewer should check that the reconciliation truly supports the balance and isn’t just rolling forward last period’s numbers. - Focus attention where the risk is highest

Accounts like cash, AR, AP, inventory, and key accruals should usually be handled with the highest priority, because errors there have the biggest impact.

Common challenges in balance sheet reconciliation

Spoiler: a lot of the problems here come down to manual workflows and a lack of structure. Even though reconciliation is a fundamental control, it isn’t always easy to execute well. Many finance teams often run into recurring challenges:

- Spreadsheet risks: When reconciliation’s done in spreadsheets, formula errors, missing items, or simple copy-paste mistakes happen. Over time, these ‘small’ issues can have a big impact on the balance sheet’s integrity.

- Inconsistent processes: If reconciliations aren’t handled the same way each period, or if procedures aren’t clearly defined, controls can break down and cause reporting problems.

- Heavy documentation work: Gathering evidence, attaching support, and documenting explanations can take up a surprising amount of time during the close.

- Limited visibility: If reconciliations live across a blend of emails, shared drives, and individual files (old habits die hard…), it’s difficult for leadership to see which accounts are finished, in review, or still outstanding.6

- Scaling problems as companies grow: As transaction volumes increase, manual reconciliation processes often struggle to keep up, raising the risk of missed issues or delayed reporting.This is especially true for multi-entity organizations, where intercompany reconciliation adds another layer of complexity — requiring balances to match across subsidiaries before consolidation.

Best practices for handling the process effectively

Balance-sheet reconciliation works best when it follows a clear, consistent structure. One of the first steps is setting up formal policies that define which accounts need to be reconciled, who should prepare them, how often they should be completed, and what supporting documents are needed. Having these rules in place keeps the process consistent, even as companies and responsibilities change.

A risk-based approach is also important. As we mentioned in the step-by-step overview earlier, higher-risk balances – cash, AR, AP, inventory, and major accruals – should always be reconciled before the close. Depending on your business’ size, lower-risk accounts might sometimes be reviewed using analytical checks instead of a full reconciliation.

Strong internal controls also depend on a clear segregation of duties. Meaning that, ideally, the person responsible for processing transactions isn’t the same person preparing or approving reconciliations.

Timing matters too. Reconciliations should be completed while the accounting period is still open – so if you need to make any adjustments, they can be posted before financial statements are finalized.

Finally, bringing technology on board makes reconciliation more efficient. Automation can handle routine data collection and matching, so accountants get more time to focus on investigating unusual or complex items.

The future of balance sheet reconciliation

Balance sheet reconciliation is gradually moving beyond the traditional month-end routine. Many finance leaders are now working toward a “continuous close” model – meaning reconciliations and control checks happen more regularly, instead of being compressed into a few busy days at period-end.

Several trends are pushing this shift:

- More automation in everyday processes: Routine matching, roll-forwards, and data gathering can run continuously rather than waiting for month-end.

- Predictive tools that flag issues early: AI models can identify unusual balances or suggest potential reconciliation matches before teams even start the close.

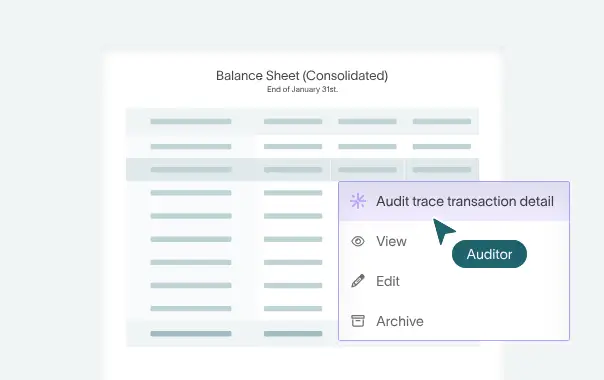

- Stronger digital audit trails for ICFR: Regulators increasingly expect reconciliations, approvals, and supporting documents to be clearly recorded and easy to trace.

- Broader reporting needs: New sustainability and ESG reporting standards depend on reliable financial data – which starts with well-reconciled balances.

We’re looking toward a future where the routine parts of reconciliation happen automatically. Finance professionals' jobs are changing fast: there’s an increasing focus on reviewing exceptions, interpreting results, and tackling strategic work rather than manually matching transactions.

Where AI and automation fits in

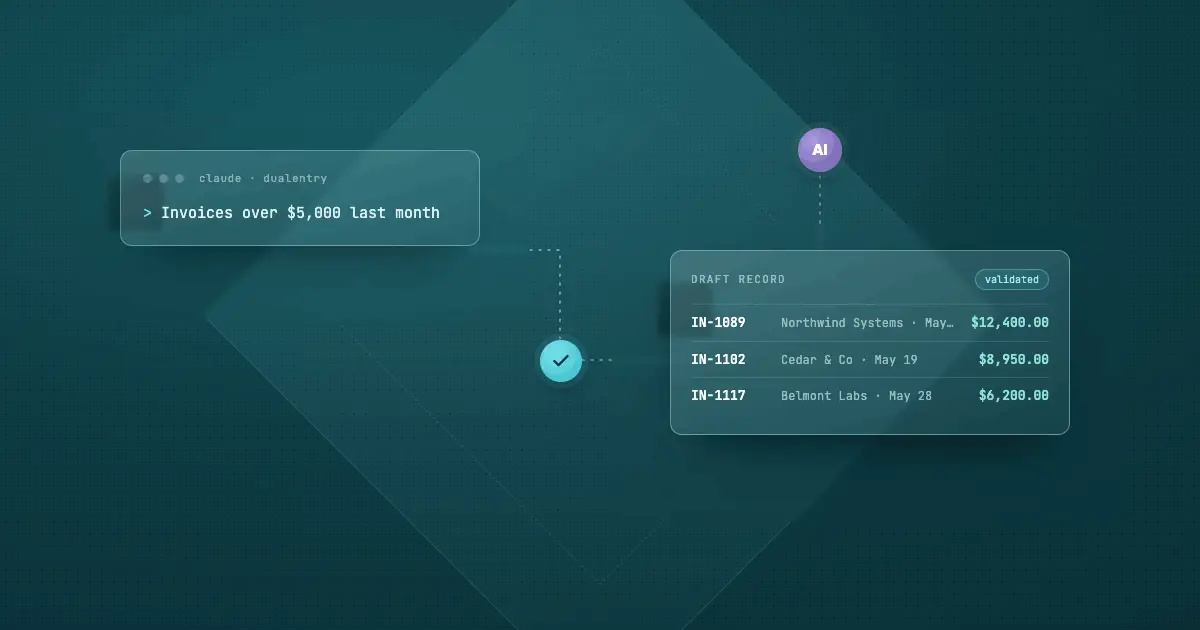

AI and automation are changing how reconciliations are handled. To save accountants from manually comparing thousands of transactions, software can automatically collect data from ledgers, subledgers, and external sources, then apply matching rules to reconcile most items hands-free.

AI-powered platforms take this idea further by recognizing patterns in historical reconciliations. Over time, they learn how transactions typically match and can suggest pairings even when amounts or references aren’t perfectly identical. Automation also improves exception handling, only flagging up items that genuinely need investigation, like unusual balances, missing entries, or duplicate transactions.

Of course, this all has a big impact on the close process. As more reconciliation steps are automated, companies can shorten reporting cycles, put last-minute adjustments in the past, and feel more in control, keeping track of the process in real time.

How Dualentry simplifies balance sheet reconciliation with automation

DualEntry brings structure, automation, and visibility to reconciliation. You can validate balances faster while keeping strong controls – and robust documentation to match.

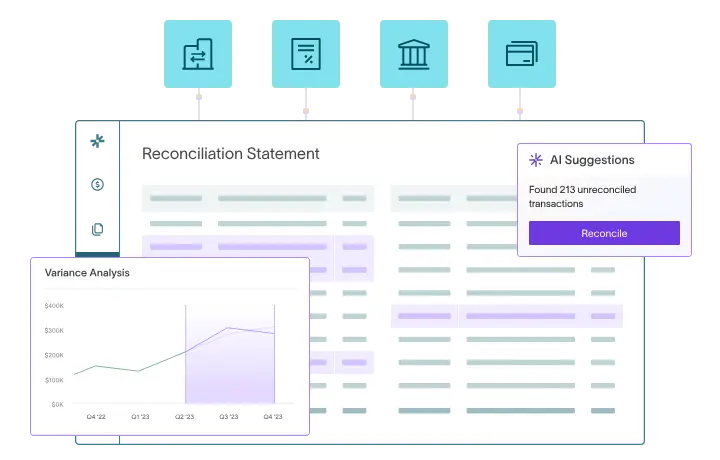

Automated high-volume matching: DualEntry can process millions of transactions across multiple accounts at once, automatically matching entries one-to-one, many-to-one, or many-to-many.

AI rule creation and smarter matching: The platform learns from past reconciliations and suggests custom matching rules, helping to improve accuracy and reduce repetitive manual work.

Exception management and anomaly detection: Instead of combing through every transaction, DualEntry highlights the unusual patterns or unmatched items that actually need investigation.

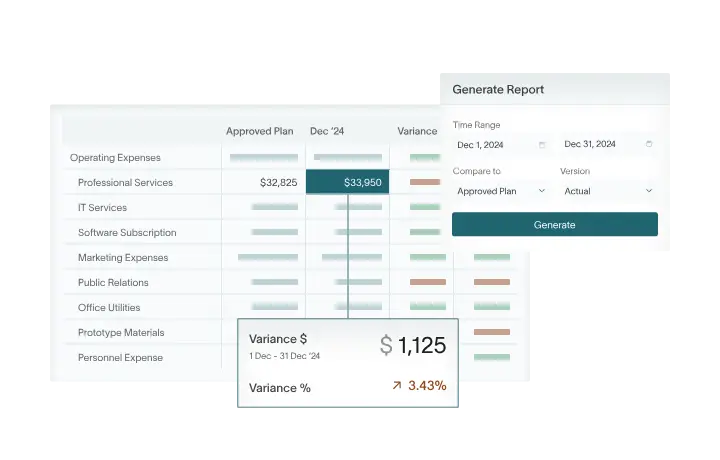

Flexible reconciliation templates: The platform lets you choose from standardized templates or customized schedules – whatever best helps you keep reconciliations consistent across accounts and entities.

Automatic roll-forwards and historical period control: Reconciliation schedules carry forward between periods automatically, while still allowing you to review or adjust historical balances when needed.

Real-time dashboards and workflows: You can track which reconciliations are prepared, reviewed, or overdue in one place, with clear approval workflows and full audit trails.

Balance Sheet Reconciliation FAQs

Conclusion

Balance sheet reconciliation plays a crucial role in keeping financial operations disciplined and transparent. When you can handle reconciliations consistently – and support them with clear evidence – it doesn’t just make regulators and auditors happy, but it also makes your team’s day-to-day work and decisions stronger.

In the age of AI accounting, the way this work gets done is, of course, changing. Automation is helping teams move away from spreadsheet-heavy processes and into more structured, reliable workflows that flag up issues earlier and reduce manual effort.

DualEntry helps put these improvements into practice by bringing standardized reconciliation processes, approval workflows, and intelligent matching directly into everyday finance work.

Schedule a demo to see how DualEntry AI can support a more controlled, scalable approach to reconciliation – without adding complexity to your close.

See the full power of DualEntry in 30 minutes

Do San (Justin) Myung

Expert Accountant & Former Consulting CFO | DualEntry

Justin (Do San Myung) is Expert Accountant at DualEntry with 20+ years of hands-on experience managing general ledgers, financial close processes, and ERP implementations for mid-market and enterprise companies. As a former Consulting CFO and Controller, he has personally overseen month-end closes, SOX compliance programs, and multi-entity consolidations across technology, manufacturing, and services industries. Justin specializes in transforming manual accounting workflows into automated, AI-driven processes.